Part of purchasing a new home is really understanding what you can truly afford. And while you can certainly do your personal calculations on the back of an envelope (or in a spreadsheet as discussed in an earlier post), the reality is that you can only borrow what a bank or lender is willing to underwrite you for. So as you get started on your home search, getting a mortgage pre-approval is an important and serious first step. Not only will it help guide what your expectations are for a future home, it signals to a realtor that you’re a serious buyer and ready to move forward.

First thing is to have a basic financial plan (Step 1 in this series of posts) on the down-payment and mortgage amount you’re interested in as discussed earlier. Next thing is to go find some lenders to work through the pre-approval process. While it’s a fairly quick process, there is some paperwork to do so I’d certainly keep it to under five different options. Trust me, you’re going to get a lot of emails and phone calls once you start this process so don’t get pre-approvals from a ridiculous number of banks.

Once you have your basic financial plan, who do you reach out to? Your existing banks and credit unions that service your savings and checking accounts is one option. Another option would be online mortgage specialists like Rocket Mortgage or GuaranteedRate. Mortgage interest rates vary quite a bit so it’s wise to speak to several banks and have some options. Both Nerdwallet and US News and World Report have good summary pages for mortgage lenders and their service ratings. Note that your realtor may also have a suggestion but we’ll discuss those relationships in more detail in the next chapter!

To start the pre-approval process, you’ll need your basic financial information: salary/earnings, assets and debts along with your current mortgage situation. For the pre-approval process, that means you’ll need to start gathering up all the relevant financial information for you and whomever else will be applying for the mortgage. One key component of the pre-approval process will be your credit score. Hopefully you’ve been working on improving your credit score before your home search. Just be aware that the credit score used for mortgage applications are often older ones that are more demanding and conservative it its calculations. For a pre-approval, you’ll need your expected down-payment amount along with the loan amount (in the high end of your range). In most scenarios your pre-approval will be handled online and you should get an answer within hours or at worst, days.

Assuming you’re pre-approved, you’ll receive a letter validating the basic numbers and you can now engage a realtor with some confidence. You’ll also get a better idea of what the bank or lender will be looking for when you move towards the final approval. Salary, wages, assets, debts, current living expenses, debts and more. It’s the start of creating your digital financial records archive in primarily image (.jpg) and document (.pdf) formats.

To help prepare these financial records, first identify all the necessary sources of your financial information: Banks, investment accounts, payroll provider, filed tax returns, current mortgage lender. Then you’ll either use a scanner, smartphone, computer print screen for the document images. Printing to pdf is another good option for creating text documents that will be best for the long and detailed home purchase process. For example, my home equity loan banker, mortgage lender and realtor all use online tools to securely request and store these financial documents, securely. And .jpg and .pdf are the most commonly accepted file formats.

When you save your personal and financial documents I recommend using a consistent naming convention for your files. I will suggest: FirstName LastName – DocumentType – DocumentSource – DocumentDate as an option. The more detail in the file name will help the people working on your paperwork given they will have multiple clients. Also when transmitting and sending documents to others, be particular cautious given standard emails are not encrypted and sending sensitive personal information (PI) by email is not a good idea.

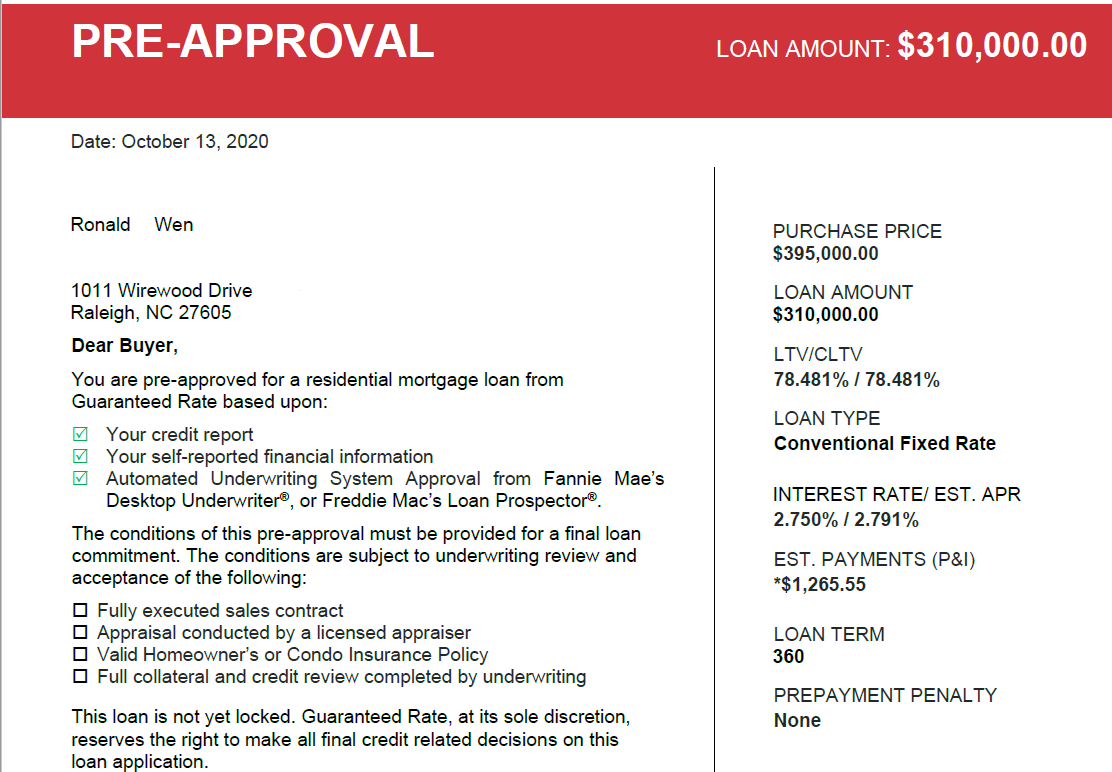

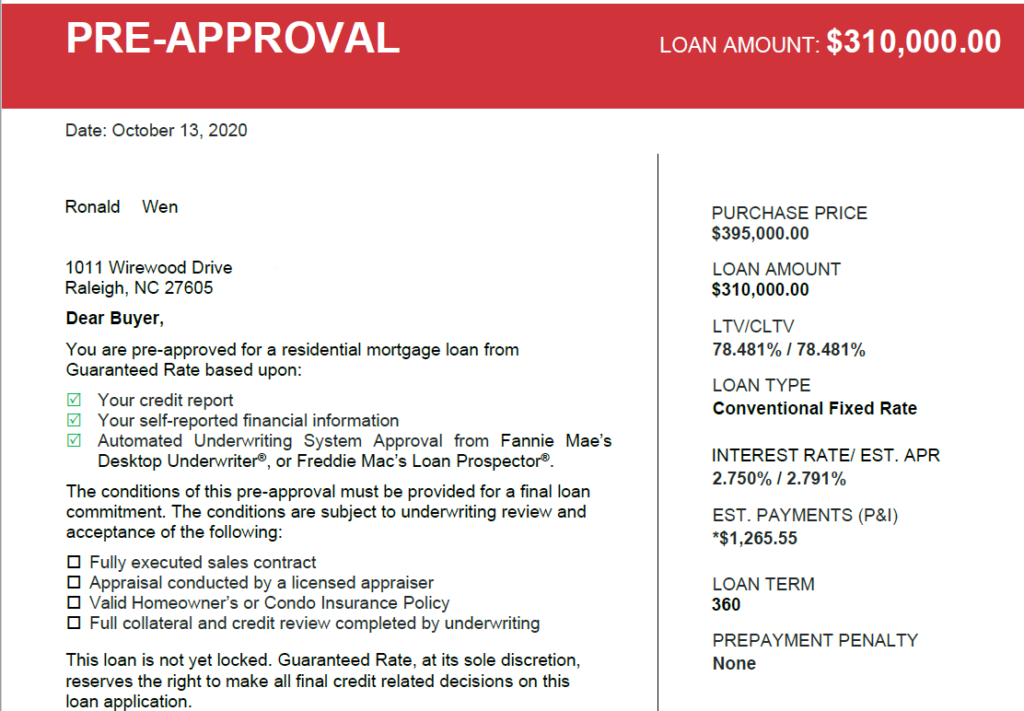

I’m including some real-life examples of the financial and personal documents you will need to get through the home purchase process. So get ready for this ride by getting all your ducks in an order! In the next installment of this series, we’ll be discussing how to choose a real estate agent.

- Payroll pay stubs

- Drivers license

- Previous filed tax returns (1040, 1095)

- W-2 from previous two years

- Bank account, savings account, investment account statements (2 months)

- Mortgage statements

- Property insurance declaration pages