So you’ve finally decided to buy a home! Like many in 2020, low mortgage rates, working from home and the pandemic has gotten people thinking about jumping into the home ownership pool. Or maybe you’re just tired of paying rent but either way, you think you’re ready. The next step is doing some 25,000 foot research and starting to narrow down your home choices. And here’s where the unfortunate reality of your finances meet the real world market! And also when you start spinning up your spreadsheets and lists to help document and prioritize your home needs. If you’re a single person like myself, hooray, the decision-making will be quicker and easier but you’ve only got one salary. If you’re a two-earner couple, hooray, you’ll have more money to spend but making the decision with two opinions will be tougher.

First thing I’d recommend doing is targeting when you want to purchase your home within a four to eight week window. Take into account any life events, the seasonality of the real estate market, weather and time to prepare your home and finances for the move. By setting up a target time period you can back into all the other details and when they need to happen. Things like when you need to get pre-approved, when you need to have the due diligence money saved up, when you need to have the down-payment ready to go, when you need to put your home on the market (if you’re selling) and when you’ll be moving. And you know that the real estate market is typically hottest from March to September with the most homes on the market but also, the most competition and higher prices. Be realistic about when you can get all the prep done on your end and how long the search will take, I’d say 1 to 3 months for a home search is realistic depending on how demanding you are.

Step two, figure out how much of a down payment you’re likely to put down on your future home. That down payment may come from cash in your bank accounts, a gift from a relative, a loan from your 401k or current house, or sale of your existing home (equity). Just be aware that your down payment will potentially impact your mortgage rate and future monthly expenses because less than 20% down on a house will incur PMI (mortgage protection insurance), which can run from .5% to 1.0% or so. For my current mortgage, I think PMI adds about $90/month on a $200k mortgage. We will talk about mortgages and personal financial history in more detail later during the pre-approval process!

Step three, do a review of your finances to determine how much house or home you can afford on a monthly basis. There are two numbers here, in my opinion. The traditional rule for home buying is 28% of your gross monthly income at the higher end. In most average markets, that 28% should be plenty but I’m thinking that in high housing expense areas like California, NY, Boston, etc, you may have to be paying out that much or more, unfortunately. At the lower end, I’d put down what you are spending today for your living situation with the expectation to pay more when you’re purchasing a home.

So now you have an approximate range of what your monthly home expenses could or should be. Plug those numbers into your monthly budget (hopefully you have one) to make sure you feel comfortable at either end of that range. If you’re under 50, you can anticipate your earnings to increase over time. But mentally set a range of what you’re comfortable with in terms of home expenses, these numbers are still pretty broad but will help us figure out how much home you can afford.

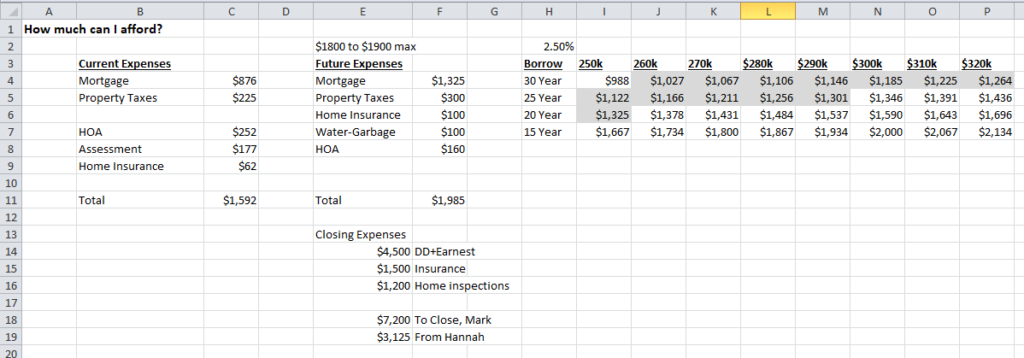

Step four, let’s figure out how that monthly living expense translates to a target property value. Use a mortgage calculator, interest rate (be conservative here, choose a 30 year fixed interest rate) and range of money borrowed to see what the monthly “mortgage” could be. In the image above, I have a range of borrowed mortgage amounts across four different mortgage loan lengths (from 15 to 30 years, assuming a fixed rate). I then plugged in amounts from the mortgage calculator for each possibility. My expectation of a mortgage costing $1,000 to $1,300/month is shaded in gray. That’s a baseline for how much you’ll spend but there will be additional expenses like property taxes, property insurance, water-sanitation-refuse fees and HOA fees which becomes a more realistic, future monthly expense. These are line items that you may not pay right now, as an apartment person who rents but you will, once you purchase a home.

You now have a fairly accurate expectation on what your monthly home expenses will be at various amounts of mortgage money borrowed. When you add your down payment amount to the money borrowed, you’ll have an approximate home value for each monthly home expense! In my case it was $320k to $390k given an expected down-payment of $70k and mortgage of $250k to $320k. The range of what you can afford on a monthly basis defines how much you should-can borrow. And that amount in addition to the down-payment becomes how much home you can buy from your perspective. Once you apply for a mortgage, the number could be slightly different from your own expectations since they will take a deep-dive into your financial situation and determine, what they are willing to lend. And as you can tell, there’s a lot of math and modeling in the home buying process. And since a lot of these calculations are estimates, you should try to be conservative when you model what you can afford.

Realistically for me, I had a range of $300k to $400k for my future home with a target price of $375k based upon my initial financial model. A number where I thought I could get a decent house with a decent amount of space and not feel too stressed financially. My current condo is valued at about $300k so a larger, more valuable home is the overall goal (gotta move on up)! In a high cost real estate market, I could see someone ratcheting their target numbers down a bit to keep things affordable but that’s your call.

But there are still a lot of questions to be answered even with those target home price numbers. Do I get a detached home or townhouse? How big should the home be? Which locations are a good fit? What features do I want to have vs. I have to have? That’s the next step once you’ve calculated the basics of what you can afford. The price range you can afford will be one of the key criteria for when you set up your online home search to find properties for sale. Before we even get to that point, let’s talk about the down-payment needed in our next Real Estate 101 blog post!

Resources