If you’re a first-time home-buyer, there’s so much to learn for maybe the biggest purchase of your life. And you need to learn things stat, to make better decisions and minimize poor decisions throughout the home-buying process. Setting up your initial house budget and figuring out how much home you can afford, getting a mortgage pre-approval, financing your down-payment and estimating your purchase timeline, to choosing a realtor. All very important things to do before you even step out the door.

Now here comes the fun part, searching for and visiting homes on the market! After you sign a contract with a realtor as an exclusive agent, they will most likely set up an automated search on MLS listings to let you know what is for sale and what is coming onto the market. If they’re really good, they will keep you appraised for what’s COMING to the market. Given how hot real estate is in 2021, you have to get a head-start to succeed.

Here’s where they information you gleaned from targeting a home will come into play. Usually the search is based upon several major criteria: price range, home type (house, townhouse, condo, duplex), location by city/zip code, square footage and age. When you start your search you should have a pretty good idea of what you want in your perfect home so these guidelines will help your realtor deliver listings of interest to you.

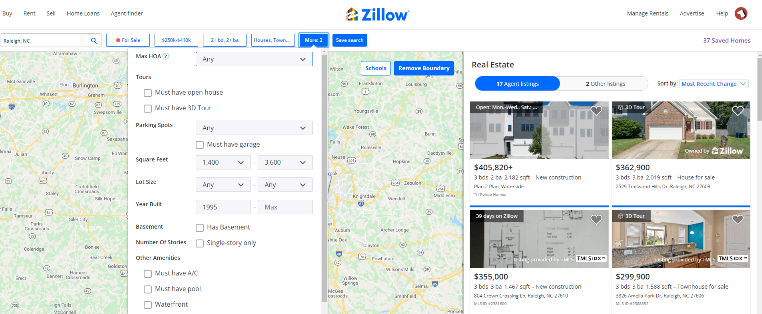

But in my scenario, I had already been stalking homes for months before I even engaged a realtor. While your realtor will use a professional MLS listing application, I found that Zillow does a darn good job and has some nice features. You can set up a custom search just like your realtor will but on the Zillow app, you can also draw a boundary line map for where you’d like your listings to come from. This map feature is a much better way to target homes if you know what you want. I created one primary search based on fairly exact numbers of what I can afford and wanted within this mapped out zone. I then created a broader search that had larger boundaries, a bigger price range, bigger square footage range, bigger age range, just in case I was missing out on something.

Some other things to consider researching beyond MLS listings is a crime map, school map and flood plains maps. These are three necessary categories of information that may not be apparent in a house listing. Crime maps will give you an idea of why a neighborhood might be so cheap. School maps and ratings may be important if you have a child in school or getting ready for school. Flood plain maps will tell you how likely your home might be inundated if a creek or river overflows. Unfortunately with global warming, we’re seeing more and more of that happen so be warned. You can expected higher and more expensive home insurance premiums if you choose a home in or near a flood plain. I also had a map to identify future construction projects which will give you some ideas of areas that might become more attractive over the years.

In regional markets that are hot and MANY are right now, you better be ready to move quick. Try to visit in the first couple of days that a home is listed to be competitive. You’ll probably have maybe 25 minutes to check out that home and that may be ALL you get before you have to make an offer. My realtor told me that on average, home-buyers visit 12 to 15 homes and over time, your mileage may vary based upon your comfort level. Just realize that as a first-time home-buyer, you can’t expect a perfect home in today’s hot market. Given it’s one of the biggest investments in your life, I know it’s a REALLY hard decision to make that quickly.

When you visit a home, you’re going to notice a lot of different things and over time and visits, you’ll start to tune in on what’s important. Condition of the carpet, interior walls and doors are important. Think of how much life they have left and when you might have to replace them. Windows and window treatments? If you don’t like them and need to replace the, the price adds up quickly to the thousands of dollars. Lights, ceiling and mouldings, are they attractive to you (smooth or popcorn ceiling) and is the over the head look and feel acceptable? Appliances, are they in decent shape, good brands and about how old are they? Kitchen counters, cabinets, bathroom fixtures and bathroom cabinets. Is there enough space? Have they been updated? Not everything needs to be perfect but get an idea for what you can live with and the potential cost it will be for you to update things.

Landscaping? Is the lawn and yard manageable? What’s the grade like for your yard and lot? Preferably, water flows away from your home and foundation, rather than pooling up near your structure. HVAC, is it in good shape and how old is it? AC and heating units are some of the most expensive items to replace or update, take care here. And finally the siding and roof? How old are they and in what condition? Usually 25 years is to be expected for a lifespan, do your due diligence.

All these questions and answers should be ticked off as quickly as possible as you visit the home. Ask your realtor about the neighborhood vibe to make sure it fits into your lifestyle. And make sure you have access to necessary infrastructure and amenities like grocery stores, highways, and more. You may only get one quick visit to your target home so make the most out of it. Once the first offer goes in, you’ll usually have 24 hours or so with your BEST offer so get the most out of your visits

I’ve said this before but in today’s hot real estate market for a newbie buyer, it is REALLY hard. I’ve heard stories of prospective buyers bidding on 3, 5 or even more properties and not getting a home. Even if a home you’re looking at is not the one for you, it will help you tune your expectations and help prioritize what features you really need vs. want. And set your expectations on what’s in your price range and affordable.

So have fun as you look through these homes and imagine yourself living in there and being part of the neighborhood. One note, if you’re inspecting a home that still has a resident, please schedule your visit the day before vs. hours beforehand! As someone who has shown their home, it’s a LOT of work to clean and vacate it for visits so some extra time is helpful. For my next post, I’ll cover putting down an offer on a target home, here’s where things get REALLY interesting… 🙂

Key Real Estate Purchase and Sales ToDos

- Targeting a new home for purchase

- Timeline for buying a home and the down-payment

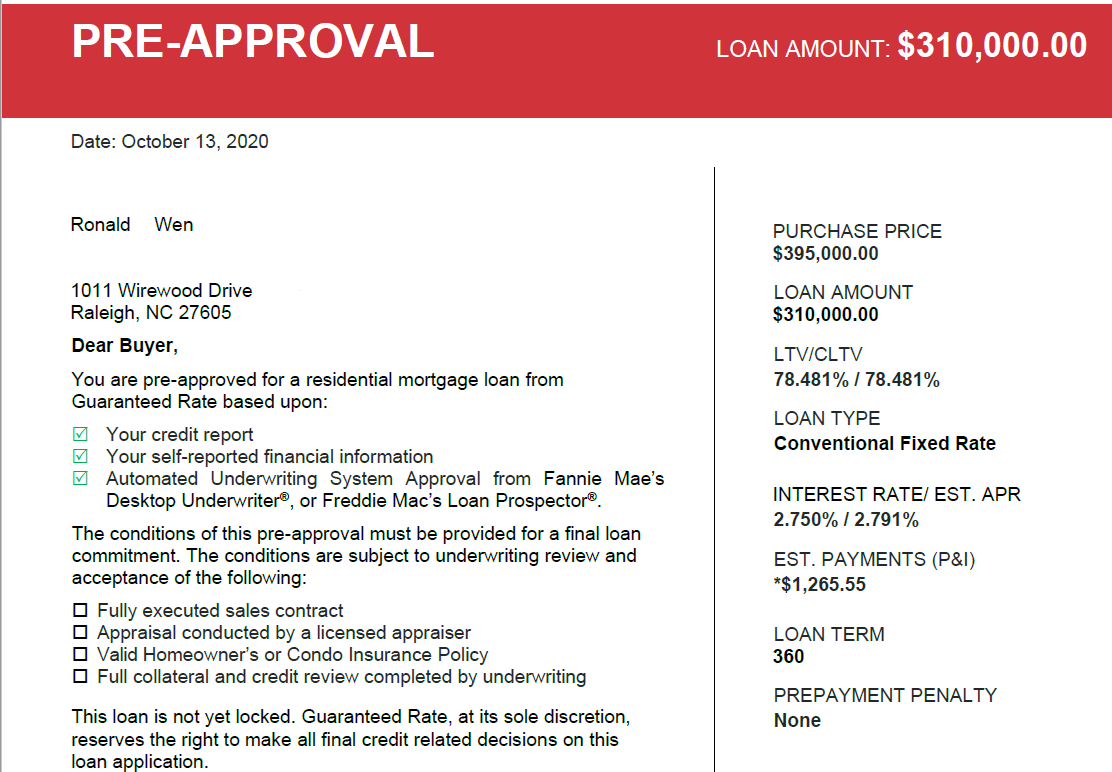

- Finding a mortgage, pre-approval and finances

- Picking an agent

- Searching for and visiting properties

- Offer – Price, closing date, due diligence, earnest money

- Due diligence, inspections and closing on your new home

- Selling your house

- Showing your home for sale

- Closing on the sale of your home