If you’ve made it to this point in the process and in this series of blog posts, congratulations! You’re ready to take the next big step, putting down an offer on your future home! And here’s where it also gets really tricky, especially in the real estate market of 2021. We’ve seen home-buying competition in a way that has NEVER been seen in decades due to a short-fall in new home building, shortages in lumber and a Millennial generation that’s ready to move out of apartments and into their first homes.

So if you’re lucky enough to find a nice home within your budget and needs, congratulations. It’s time to get to work on a real offer to that home-owner and this will require some work but time is limited AND be prepared for some disappointment. Nice homes are usually getting multiple offers and yours needs to be competitive to stand a chance. And you’ll need to have your checkbook and cash ready if your offer is accepted as discussed in Step 2.

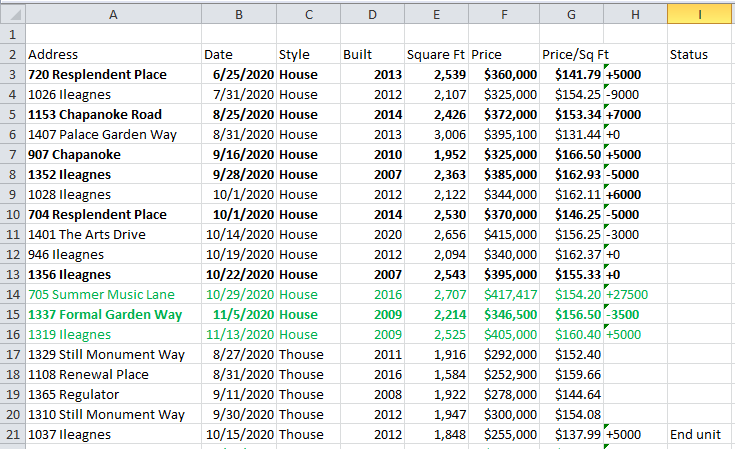

To start with, let’s take a look at comps. Using Zillow or your realtor tools, take a look at the homes in your target neighborhood over the past 3 to 6 months. Try to identify homes that are about the same square footage, same age and same condition. Pop them into your spreadsheet with those basic details and calculate the price per square foot for each similar home to your target. With this baseline number, you can estimate what your target home may be worth.

In the above example for Raleigh, I’ve got homes in my target range of $300k to $400k. And thankfully in this neighborhood, the home ages and sizes are pretty similar so the comps will be pretty accurate. You’ll have to have done this work beforehand since you’ll often have to submit an offer in short time after a house hits the market. You’ll also need to adjust based upon the specifics of your future home: Yard size, upgrades, overall condition, etc. In this spreadsheet, not only do I have the price per square foot but also documented the overbid situation. What was the home listed price and what did it actually sell for. Talk to your realtor about how hot the market is and what you may need for an over-bid situation. They will be hearing through the grapevine about what’s needed in your target neighborhoo.

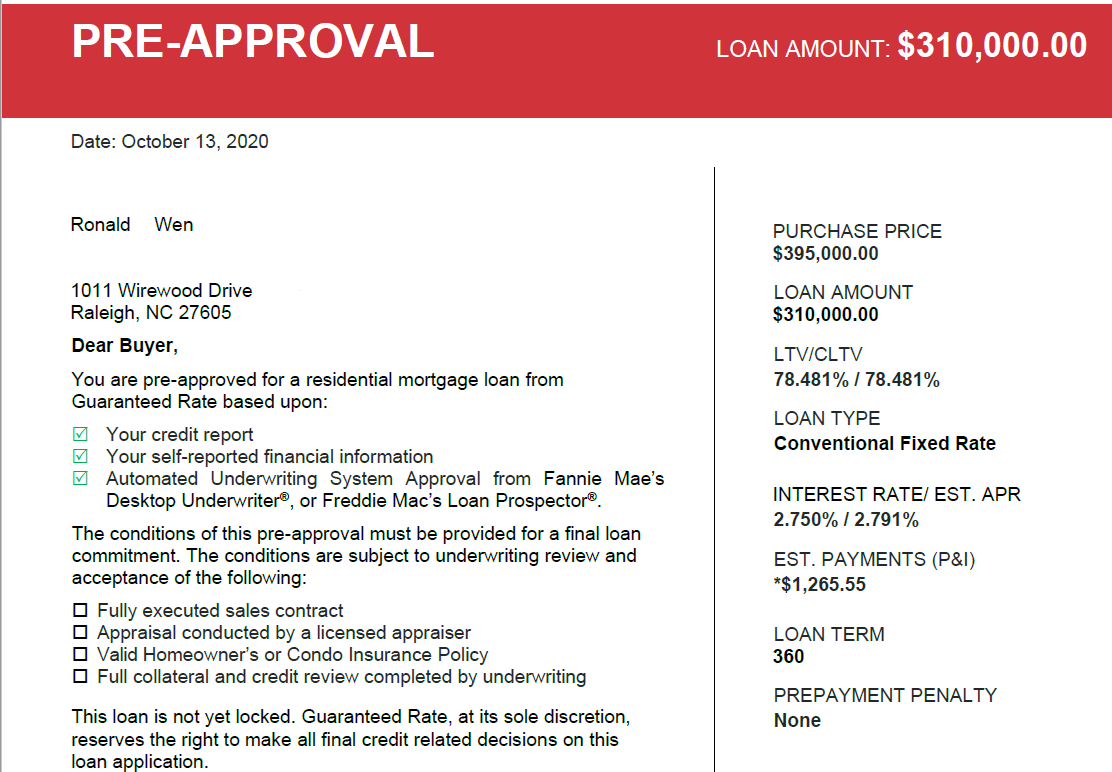

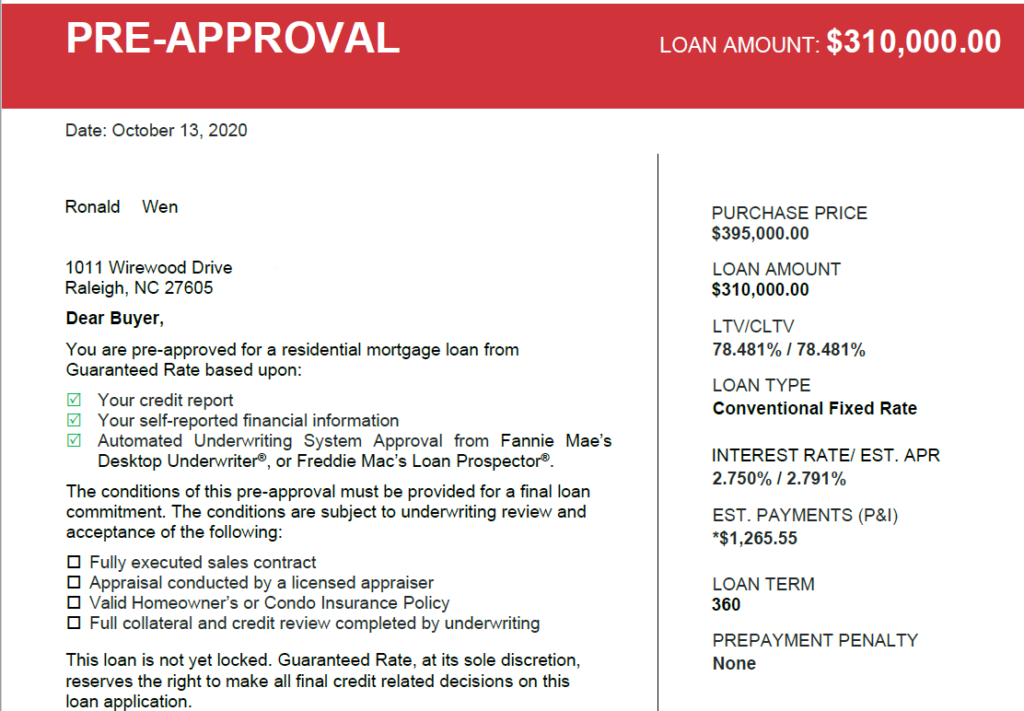

Next up is the details of the offer. You’ve established a price-value of your home but there’s a LOT more to your offer than just the sale price you’re willing to pay. You’ll need to package up all the details of why you’re a qualified buyer to position your offer, against all the other offers. Your pre-approval, down-payment size (some people are buying in CASH) along with contingencies (inspection, appraisal, loan, sale of your home), due diligence and earnest monies will all be part of the offer. And you’ll also define a due diligence period (time to inspect the home, this could be waived if inspections are waived or buying as-is) along with target close date. Note that in today’s hot real estate market, some buyers are going all in with cash and waiving inspections to purchase a home. Which means the buyer is assuming nearly ALL the risk, removing all the risk for the seller. But for most people, a contingent offer is likely.

Your due diligence and earnest money will be needed if the offer is accepted and once accepted, the listing will be pulled as under contract. Due diligence money is needed for the seller to pull the listing and give you time to do your inspections and finalize your mortgage. Earnest money is ADDITIONAL money given to the seller to show your commitment to the purchase. If you back out at any point and time in North Carolina, you give up your due diligence money after going under contract. BUT you can get your earnest money back if you back out during the usual, 2 week due diligence and inspection period. Either way, the amount of money you offer to the seller as due diligence and earnest money shows how serious you are as a buyer. In today’s hot market, these amounts have increased to seriously high numbers. And that money needs to be ready to go, you’ll send the seller a bank or personal check once you’re under contract and the monies will be held in escrow.

Once you’ve finalized the offer amount, due diligence and earnest money, your realtor will figure out additional details such as the due diligence period and closing date. You may have to schedule a mortgage appraisal visit, home inspection and land surveyor along with handling some other legal research in the due diligence period. Some sellers will want to close as soon as possible (if they’ve already sold, for example). Others may want a longer close if they still have to find a home. In some cases there are even rent-backs where you officially purchase the home but rent it back to the seller for some additional time if needed.

As you can tell, the home offer is a crucial point in your new home search and when things really start to get sticky. You’ve gone from dreaming about your new home to finally making a commitment, both financially and emotionally. Ask anyone who has looked for a home in the past two years and you will hear tales of woe and happiness, the search for a new house will take you through many ups and downs. But hang in there! Because if your offer is accepted (fingers crossed), there is still a lot of work to do. In Part 7 of this series we’ll discuss the inspection, counter-offer and final closing. There’s still much to do but you’re moving forward!